While most analysts have given the Krafton stock (KRX:259960) a buy rating based on strong earnings momentum and decent valuations, the Korean game developer trades at the cheapest valuation among its regional peers.

Based on analyst consensus, the company’s average 12-month price target is around 352,708 to 364,320 KRW, pointing towards a minimum potential upside of over 30%.

However, my analysis concludes the rating to be a HOLD, with a price target between 280,000-300,000 KRW with a minimum 15% upside.

Krafton Trading at a Cheap Valuation

The company is currently trading at 15.7x earnings, which is one of the lowest valuations in Asia’s gaming sector, with Nexon which is trading at 23.3x, while NCSoft is trading at 15.4x. If you look at the Western competition, Electronic Arts is trading at around 74.6x.

The investment thesis for Krafton’s stock is to hold, which is down to declining MAU on PUBG, jury being out on PUBG 2.0 migration powered by Unreal Engine 5, in-game monetization issues and the company’s present inability to diversify its portfolio that can shoulder a decent chunk of its annual revenue.

However, the current trading valuation isn’t an anomaly – Krafton stock is cheaper because the company’s entire value proposition revolves around a single IP.

If you take out the other revenue segments and the advertising revenue generated by its subsidiaries, PUBG accounts for 97% of the company’s core gaming business.

On top of that, it is the mobile version where PUBG goes the furthest, racking up 1.74 trillion won in revenue in 2025, with the PC and Console versions revenues seen more as rounding errors than being significant contributors.

However, the biggest risk to the company is not the mobile revenue dominance – it is the IP’s maturity or lack thereof.

The franchise launched in 2017 ahead of the 2018-2020 period which is considered a peak era for battle royale genre. Today, the same genre is experiencing a decline in popularity, with focus shifting toward “sandbox” gaming.

To stay in tune with the evolving market trends, Krafton spent $160 million plus on The Callisto Protocol, a survival horror game. However the game pretty much crashed and burned. inZOI and MIMESIS sold 1 million units each but accounted for only 3% of the total revenue.

Since PUBG, no IP has proven to be a product that can contribute $500 million plus in annual revenue potential.

PUBG 2.0 to Change Things?

The company is currently working on expanding its PUBG content through an Unreal Engine 5 upgrade, which can potentially increase the game’s lifecycle to at least three years. As a consequence, it could contribute positively to the stock price.

However, a failed attempt could potentially be a final nail in the coffin of an IP that is struggling to hold its own in a changing landscape.

The jury is still out whether PUBG 2.0 will flip the script so until the beta data does not offer a reliable proof of concept, the stock is likely to continue trading on the cheap. There is of course a modest upside but more information is needed to see whether the upside will improve.

Is PUBG Nearing the End of a Cycle?

Looking at how the battle royale genre has fared in recent times, there is a sense that PUBG has already peaked and any bit of revenue the company generates through the game would purely depend on stable MAU growth.

While the 2.0 upgrade does sound like a good plan, it is still unlikely to sustain player interest.

Using the recent closure of Call of Duty: Warzone Mobile is a good way to back up this thesis. The game experienced a significant decline in both userbase and revenue, despite garnering over 100 million downloads but shut down earlier this April.

Having played the game myself, I believe the biggest issue with COD: Warzone Mobile was a lack of content variety, with the developers more focused on keeping it similar to previous iterations with minimal unique mechanics and systems.

So the question is, can PUBG 2.0 separate itself from its existing version and move away from a pay loot system that could be impacting player retention in recent years?

However, looking at its recent numbers, it doesn’t look like that PUBG is in a state of decline.

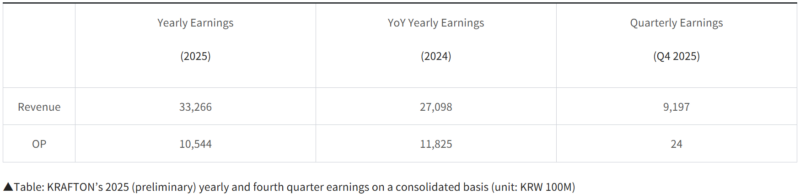

Looking at the company’s revenue breakdown, it is quite evident that while the 2025 numbers showcased growth across mobile and console platforms, revenue fell across all platforms, led by mobile where revenue fell 40% year over year in Q4, 2025.

Similarly, operating profit fell 11% year over year, reflecting the company’s investment in PUBG 2.0 development.

What perhaps sets PUBG apart from the likes of Fortnite and Warzone is its lower hardware requirements which allow it to potentially enjoy greater penetration as it looks to expand across other regions.

PUBG 2.0; The Bull and Bear Case

The Bull Case

Perhaps the biggest catalyst to trigger a bull case scenario would be the company’s ability to come up with a visual upgrade and in-game depth that attracts players who walked away due to aging graphics. Powered by Unreal Engine 5’s capabilities, the new version could be a key differentiator.

Understanding customer psychology and behavior is also critical. What Fortnite currently does well is that it ALLOWS players to spend money on elements such as progressive skins, colored smokes, special car skins etc. This is where PUBG’s in-game monetization strategy has room to grow. Sort that out and perhaps it will have an impact on MAU growth over time.

Making these changes could have an impact on the stock which will then re-rate to around 15-18x, backed by extended lifecycle potential.

Bear Case

As can always be the case in such instances, migration to Unreal Engine 5 results in bugs and overall performance degradation. Compatibility issues surface which gives way to players leaving the platform. This isn’t a new thing – several AAA titles have botched this.

Visual fidelity isn’t necessarily the key driver for an average PUBG user – those who have been playing the game for several years, prioritize mechanics, maps and tactical positioning over visual appeal. An upgraded game solely focused on visual appeal without revising the in-game monetization strategy means that the company isn’t just leaving money on the table, it is accelerating a genre fatigue that battle royale games are already experiencing.

This could lead the way for a terminal decline, highlighted by revenue erosion, with Krafton trading on 6-8x valuation.

Trading Cheaper Because of Low Diversification

The company’s current twelve month trailing P/E ratio is a discount to its local competitors because let’s be honest – market gives credence to a diversified portfolio. Krafton isn’t necessarily trying to be a company that relies on a single game to increase revenue, recent game launches haven’t really made a huge difference to company financials.

The Callisto Protocol failed. The game launched at $60 and grossed $120 million. After platform fees, the game coughed up around $84 million, generating a loss if you take into account development and marketing costs.

inZOI entered the market in 2025 as a competitor to The Sims franchise. In the first week, the game booked around 1 million units but in reality, it was a mere drop in the ocean since its price point and platform fee meant that the game made less than 1% of the company’s annual revenue.

Conclusion

In short, the entire Krafton investment thesis rests on its ability or inability to stabilize MAU growth for PUBG, well-executed PUBG 2.0 migration, evolution of in-game monetization strategy and ability to diversify its portfolio that contributes more to its overall revenue.

Rating: HOLD

That’s a really interesting point about the reliance on a single IP. I’m curious to see how diversification might impact their long-term strategy.