This article was first published on Seeking Alpha

Summary

- CD Projekt (WSE:CDR) boasts a fortress balance sheet with zero debt and PLN 1.32 billion in cash, but trades at a demanding 42x trailing P/E.

- The investment case is highly leveraged to The Witcher 4, expected post-2026, with no new major revenue catalysts until then.

- Free cash flow and development cost management are critical as CDR relies on back-catalogue sales during the multi-year development cycle.

- I maintain a Hold rating, citing asymmetric risk/reward until a credible Witcher 4 release window or a price correction emerges.

CD Projekt S.A. (OTGLF) is currently trading at nearly 59x, which means that the company’s existing financials seem sound on the surface, with investors paying a premium for the stock. However, I would be remiss to not bring out the elephant in the room – the company’s announcement on the exact launch of The Witcher IP, which serves as the basis of my investment thesis where I assign a Hold rating to the company’s stock.

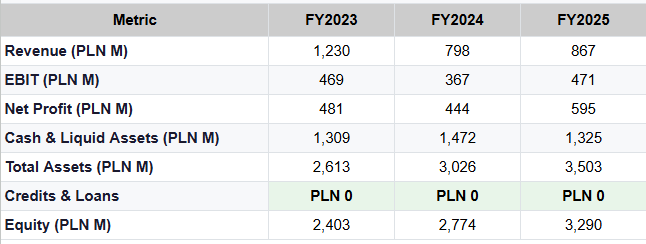

With PLN 1.32 billion in cash and liquid assets and zero debt, on the surface, Poland-based CD Projekt can stake the claim of having the healthiest balance sheet in European gaming.

In 2025, the Witcher IP and Cyberpunk 2077 revenue surged 8.6% year-over-year. Net profit zoomed 33.9% to PLN 594.7 million. Such numbers would normally mean that the company is heading in the right direction.

But upon deeper inspection, the company’s entire investment case rests on a single title, which could release around 2027. However, to date, the company has not put an exact date around the release but has confirmed that the game is unlikely to release in 2026.

The balance sheet strength and franchise equity look fairly strong, but a Hold rating makes more sense until the company provides a release date for Witcher 4. The share price also needs to be corrected based on the development timeline risk that video games run these days.

The Back-Catalogue Revenue Problem

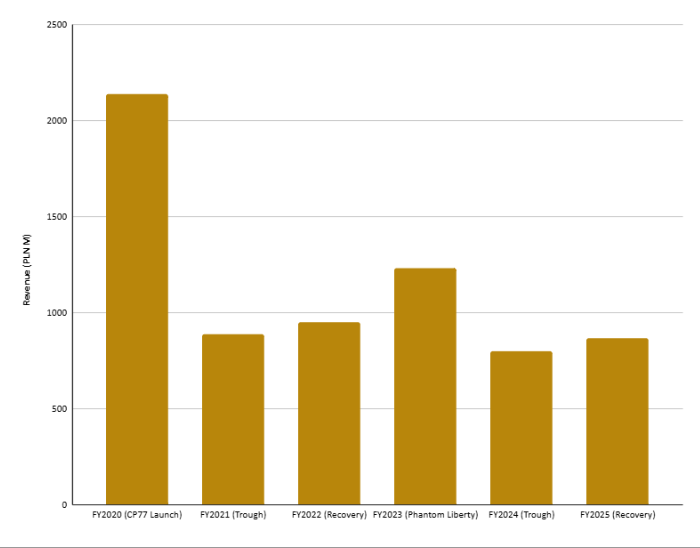

The company’s performance during 2023 is a clear example of how revenue tends to shoot up during a release window. In 2023, the company launched the Phantom Liberty DLC.

The game helped the company generate around PLN 1.23 billion in revenue, selling over 5 million copies between its release date on Sept. 26, 2023, and the end of 2023.

In 2024, however, with no new titles released, the company’s revenue shrank to PLN 799.6 million from PLN 1.04 billion a year earlier.

Revenue recovered in 2025 to PLN 867 million, but it is interesting to note that it was driven purely by back-catalog sales led by Cyberpunk 2077 and Witcher 3.

It is quite evident if we look at the figures since 2020. The company’s revenue shoots up during launch years and then normalizes when it relies on back-catalog sales. Currently, 2025 can be seen as a back catalogue recovery time period.

Based on the revenue oscillation in the last five years, the key metric to analyze would be the company’s free cash flow during its development period. A major portion of CD Projekt’s R&D expenditure was capitalized during development phases, which means that reported earnings seem to be higher than cash profitability.

Currently, Witcher 4 is passing through a development phase where the company is likely to be burning cash. Therefore, monitoring the company’s capitalization dynamic on a quarterly basis could be a more effective metric to track.

Since 2023, the company’s total assets have grown to PLN 3.50 billion in 2025, which is in line with the Witcher 4 development costs.

The company’s cash position of PLN 1.32 billion is backed by zero credits or loans, which is what potentially ends discussions of a sell rating.

The Witcher 4 Timeline

Management confirmed in 2025 that The Witcher 4 premiere is scheduled for after 2026, which consequently resulted in a 13% share price decline. Looking at the company’s development timelines over the years, a commercial release in 2027 seems likely.

Cyberpunk 2077 was delayed multiple times before it was released in December 2020. On top of that, the company had to work for 18 months to fix the product before it became a commercial success. And while the Phantom Liberty DLC did help generate around PLN 1.23 billion in revenue, the Cyberpunk misstep set a precedent of a risk that the market cannot discount on Witcher 4.

And while the studio’s ability to deliver a successful RPG in Witcher 4 isn’t in doubt, the lingering question is about how far we are from the launch. Between now and till the launch, the company is likely to have a rising cost base and there would be a limit to the amount of revenue it can generate through its back-catalog sales.

Another critical factor in this is the launch of GTA VI. While Rockstar Games is slated to release in November this year, Witcher cannot risk launching during the same window and dilute its own sales while competing for a $70-a-game core budget against a brand that is likely to dominate the retail floor space and media coverage.

CD Projekt’s management has no control over Rockstar’s release schedule. This is a risk that can only be monitored, not managed.

The Bear, Base and Bull Cases

The CD Projekt investment case revolves around three scenarios, each carrying different valuation implications.

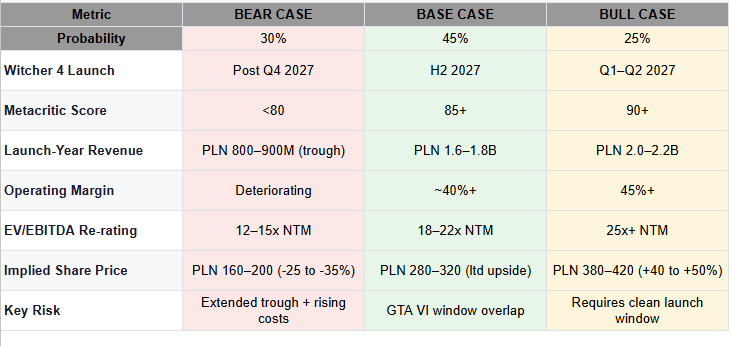

Base Case — Timely 2027 Launch (45% probability)

Witcher 4 releases during the second half of 2027 and secures a Metacritic score of 85+. Revenue improves to around PLN 1.8 billion, similar to Phantom Liberty launch year. Meanwhile, operating margins improve by around 40%. On a forward enterprise value/EBITDA basis, this projects a rating adjustment of 18 to 22x EBITDA for the next 12 months, suggesting a share price of PLN 280 to PLN320, a rather negligible upside from current levels since the stock is partially factoring in this scenario already.

Bull Case — Early Launch in 2027, Title Outperforms (25% probability)

Witcher 4 launches around the first two quarters of 2027, achieves a Metacritic rating of 90+, with first year sales crossing Witcher 3’s sales within the first two weeks. This could take the revenue to around PLN 2.2 billion in 2027. Meanwhile, the company announces a multiplayer version, providing a recurring revenue source, which could adjust the stock’s rating to around 25x NTM EBITDA and a revised share price of PLN 380 to PLN 420. The scenario would require a lot of factors working the company’s way, such as clean execution and a launch window that doesn’t come in the way of the GTA VI launch

Bear Case— Game Delayed Beyond 2027 (30% probability)

Any announcement that pushes the Witcher 4 launch beyond 2027 is likely going to have a major impact on the revenue. It is very hard to see the back-catalogue revenue sustaining beyond the PLN 900 million mark in such a scenario without the presence of a new title. There will be a domino effect with the company’s free cash flow deteriorating. The stock could also be projected to inch towards a 12 to 15x NTM EBITDA, with the marketing repricing it for an extended holding period, pushing the share price down to a range of PLN 160 to PLN 200. This would represent a 25-35% downside from current levels.

In short, the bull case offers a maximum upside of around 50%, while the bear case has a minimum 25% downside.

No Justification for Premium

CD Projekt’s current P/E ratio doesn’t compare favorably to its rivals, who have substantially more recurring revenue.

Live services accounted for around 70% of Electronic Arts’ revenue in 2025. The subscription model from Ultimate Team, Apex Legends, and The Sims creates a recurring revenue source that CD Projekt doesn’t have access to.

Meanwhile, Take-Two’s live-service infrastructure around GTA Online and NBA 2K has become a key revenue driver, based on its fiscal Q2 earnings. CD Projekt, on the other hand, is yet to build a live service product.

The decision to cancel a Cyberpunk multiplayer title to focus on the broken game issues meant that the company was forced to shelve a potential recurring revenue source. The GOG.com disposal in 2025 meant that the company is now completely reliant on revenue through CD Projekt RED. While it does simplify the equity narrative, it also removes the recurring revenue contribution which GOG provided, albeit a modest one.

The result is a business that is reliant on new launches and is exposed to execution risk, while trading at a premium compared to peers who are carrying less of the risk.

The only justification for the current multiple is purely on the belief that the Witcher 4 will be delivered on time and will be a successful title. However, that should be considered a bet, not an investment thesis, with the company seemingly putting its eggs in one basket.

What Challenges the Bear Thesis

A thorough analysis requires reviewing the strongest factors that drive the bull case.

The Cyberpunk rehabilitation counterargument is interesting. The company launched a half-cooked product in December 2020, took a reputational hit, and was forced to rebuild both the game and market trust for the next 3 years.

The launch of Phantom Liberty DLC was a success, with the game generating around PLN 1.23 billion in revenue, demonstrating that franchise equity can recover from a failed launch if the execution plan is sound. Witcher 4, on the other hand, is unlikely to launch with a credibility deficit like Cyberpunk did.

The company’s balance sheet looks strong, as discussed previously. Based on the numbers, the company has enough funds to ensure Witcher 4’s continued development without needing access to external funds.

This comes at a time when peers such as Ubisoft are facing balance sheet issues and have very limited strategic options.

Brand alignment is also on the company’s side. The Netflix partnership through The Witcher series ensures that there is sustained brand awareness across diverse demographics.

Although these factors aren’t enough to go past the 42x trailing earnings driven by a potential revenue catalyst in 2027, they do shape the narrative against a sell rating.

What Could Trigger an Upgrade or a Downgrade?

Upgrade to Buy: The company officially confirms a Witcher 4 launch date around the second half of 2027, backed by sound engagement metrics such as a strong preview score from Metacritic and pre-orders. A company statement about the successful testing of the proof-of-concept opens up multiple strategic options. A revised share price between PLN 180 and 200 would improve the risk/reward balance, compensating or offsetting execution risk.

Downgrade to Sell: A delay that pushes the title beyond 2027 and, at the same time, GTA VI confirming its launch will realign the development cost, which could also overshadow back-catalog revenue.

Conclusion

CD Projekt is a well-performing business currently stuck in an unfavorable position ahead of the Witcher 4 release. The balance sheet is the strongest in European gaming, it has maintained its franchise equity, and the company leadership has demonstrated the capacity to execute. The Cyberpunk 2077 post-launch story means that CD Projekt has the ability to fix something that is broken.

However, it still doesn’t justify paying 42x trailing earnings for a company whose next key revenue event is yet to be confirmed and has no recurring revenue products.

The scenario analysis showcases that even a timely 2027 launch carries limited upside from existing levels, while there is a meaningful downside from the bear case.

The right call could be to hold existing positions and wait for the next company update on The Witcher 4 before making your next move.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

That’s a good point about the high multiple – it does seem like investors are banking on the Witcher 4 hype a lot right now.