For investors following Take-Two Interactive Software (NASDAQ: TTWO), 2026 is shaping up to be a watershed year. With Grand Theft Auto VI locked in for a Fiscal Year 2027 launch and a freshly raised net-bookings outlook of $6.05–$6.15 billion for FY2026, the market is betting heavily that the last major pure-play U.S. video-game publisher is on the verge of a step-change in profitability. But as any seasoned investor knows, in the game industry the distance between a promising pipeline and a healthy income statement is littered with cost overruns, release delays, and studio consolidation risk. Here is what the key metrics actually say.

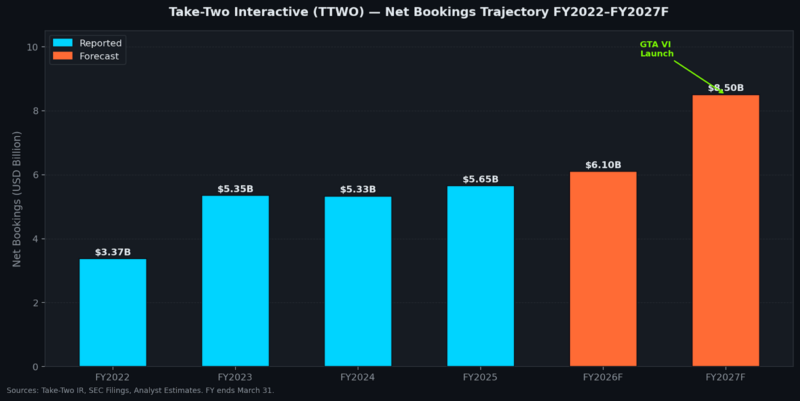

Fig. 1 — TTWO Net Bookings FY2022–FY2027F. Sources: Take-Two IR, SEC Filings, Analyst Estimates.

The Metric That Matters Most: Net Bookings

Traditional GAAP revenue is a lagging indicator for game publishers. What analysts watch is net bookings — the real-time measure of what players spend before accounting for deferred-revenue recognition. After FY2025 net bookings of $5.65 billion (up 6% year-on-year), management raised FY2026 guidance following a blowout Q1 in which bookings surged 17% to $1.42 billion, beating the top of guidance by roughly $120 million. That momentum is driven by NBA 2K, Grand Theft Auto Online, and a surging mobile segment that includes Toon Blast and Match Factory! — titles most investors still under-price.

Live-Service Stickiness: The 80%+ Rule

The single most underappreciated quality metric for a publicly-listed game developer is recurrent consumer spending (RCS) as a share of net bookings. Unlike one-time game sales, RCS — subscriptions, in-app purchases, season passes — is predictable, margin-accretive, and defensible. TTWO hit 83% RCS in Q1 FY2026, up from 78% in FY2024 and 70% in FY2022. This structural shift reduces the binary risk of any single title launch and is why Wedbush set a $300 price target in January 2026, arguing the market still under-values the live-service annuity embedded in GTA Online alone.

Fig. 2 — TTWO Recurrent Consumer Spending as % of Net Bookings. Sources: Take-Two SEC Filings.

The Bear Case: Valuation Requires Flawless Execution

The risk is real. TTWO’s price-to-sales ratio of 8.1x already exceeds the peer average of 7.6x and sits far above the broader U.S. entertainment industry median of 2x. At the same time, the company continues to report meaningful net losses — FY2026 GAAP net loss guidance of $349–$414 million, on top of heavy capitalised development costs and ongoing shareholder dilution from equity-linked compensation. A six-month GTA VI delay in a prior cycle caused a 9% single-day drop, illustrating how expensive execution risk is at current multiples. Seeking Alpha analysts note that the stock may already be pricing in the entire growth runway — leaving limited margin of safety.

GenAI and the Next Margin Driver

One newer variable reshaping analyst models is generative AI tooling. Internal adoption of GPU-accelerated development pipelines is being cited by bullish analysts as a potential structural cost reducer — cutting asset production cycles, automating QA loops, and enabling smaller teams to ship more content. Simply Wall St research tracks a modest positive revision to fair value from $277.40 to $278.23, partly reflecting GenAI efficiency assumptions feeding into higher projected return on invested capital. While not yet material, this is the kind of incremental signal that can meaningfully re-rate a high-multiple stock over a 12–24 month horizon.

Fig. 3 — TTWO Analyst Price Target Spectrum (2026). Sources: Benzinga, Wedbush, Simply Wall St (Feb 2026).

The Key Financial Metrics At a Glance

| Metric | FY2025 Actual | FY2026 Forecast | Signal |

| Net Bookings | $5.65B (+6%) | $6.05–$6.15B | 🟢 Accelerating |

| Recurrent Spending | 80% of bookings | ~83%+ | 🟢 Stickiness rising |

| GAAP Net Revenue | $5.63B (+5%) | $6.38–6.48B | 🟢 On track |

| Net Loss | ~$(790M) | $(349M)–$(414M) | 🟡 Narrowing |

| Price Target Consensus | — | $224 (range $155–$300) | 🟡 Upside w/ risk |

| P/S Ratio vs Peers | 8.1x (peer avg 7.6x) | Depends on GTA VI | 🔴 Premium |

What Investors Should Watch

Three triggers will determine whether the bull or bear case dominates in the next 12 months:

- GTA VI launch window confirmation and Day-One sales data — the single biggest re-rating catalyst in the industry this decade.

- Quarterly RCS trajectory — if recurrent spending crosses 85% of bookings, it signals a durable business model transition that justifies a structural premium.

- Net loss trajectory vs guidance — any meaningful improvement in operating leverage as GTA VI development costs wind down will be watched closely by growth-at-a-reasonable-price investors.

Bottom line: TTWO is the highest-conviction pipeline story in interactive entertainment right now. But owning it at current prices requires conviction that GTA VI will not just launch — it will redefine the benchmark for live-service economics. For investors with a two-to-three year horizon and an appetite for binary title risk, the asymmetry is compelling. For everyone else, patience may be the better trade.