Take-Two stock analysis ahead of the company’s potentially ground-breaking launch of GTA VI.

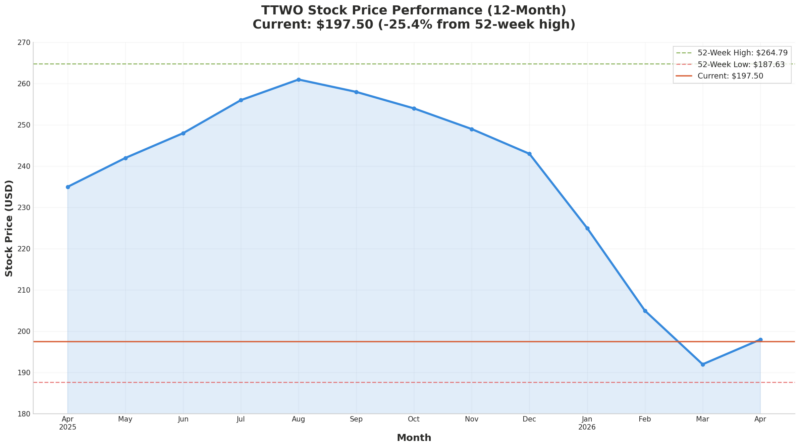

Take-Two Interactive Software (NASDAQ: TTWO) has experienced a 25% drawdown from its 52-week high of $264.79, currently trading at $197.50 as institutional investors de-risk ahead of gaming’s most anticipated launch. With Grand Theft Auto VI scheduled for November 19, 2026, the critical question facing investors is whether the recent share price weakness has created a compelling entry point or signals deeper structural concerns about the company’s ability to justify its premium valuation.

Current Valuation Framework: Trading at the Investment Trough

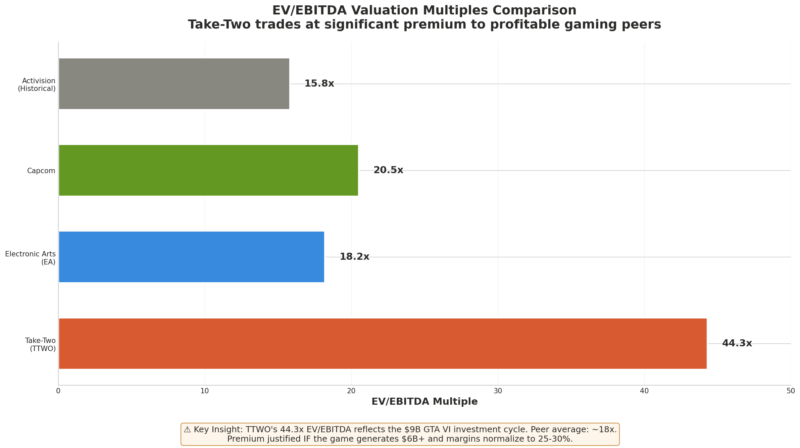

Take-Two’s equity trades at metrics that appear expensive on traditional screens but must be contextualized within the company’s unprecedented capital deployment cycle. The stock currently commands a forward price-to-earnings multiple of 102x and an enterprise value-to-EBITDA ratio of 44.3x, multiples that dwarf profitable peers Electronic Arts (31.85x P/E, 18.2x EV/EBITDA) and Capcom (29.4x P/E, ~20x EV/EBITDA).

However, these metrics reflect a company in the terminal phase of the largest entertainment development investment in history. Take-Two absorbed over $9 billion in net losses from fiscal 2023 through 2025 developing GTA VI and other major titles, creating temporary margin compression that renders trailing multiples largely irrelevant for valuation purposes.

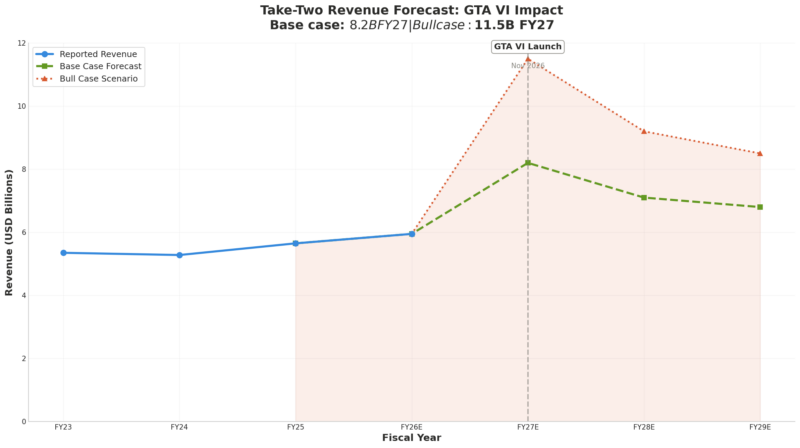

The more instructive valuation approach examines enterprise value relative to projected post-launch revenue and normalized EBITDA margins. At a current market capitalization of approximately $36.5 billion and minimal net debt, Take-Two’s enterprise value of roughly $38 billion represents just 4.6-6.3x fiscal 2027 estimated revenue of $6-8.2 billion (base case) or 3.3x in the bull case scenario projecting $11.5 billion.

Analyst Consensus: Strong Conviction Despite Execution Risk

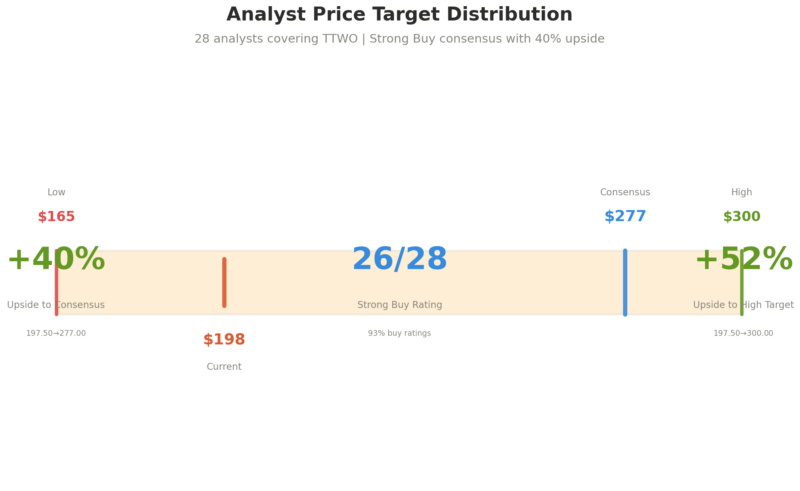

The sell-side research community maintains overwhelmingly bullish sentiment despite recent price action, with 26 buy ratings, 2 outperform ratings, 1 hold, and 1 sell among 28 analysts covering the stock. The mean price target of $276.81 implies 40% upside from current levels, with estimates ranging from a bearish $165 floor to a bullish $300 ceiling.

This wide target dispersion reflects fundamental disagreement about GTA VI’s commercial trajectory rather than company-specific execution concerns. Bears anchor to conservative $3-4 billion lifetime revenue assumptions, while bulls model aggressive $7-10 billion scenarios incorporating robust recurrent consumer spending penetration.

Wells Fargo recently trimmed its target from $301 to $295 while maintaining an Overweight rating, citing near-term macro headwinds but reiterating conviction in the GTA VI super-cycle thesis. BMO Capital Markets projects 45 million units at launch with potential $100 price points, establishing a $265 target. The institutional consensus view holds that current valuation adequately compensates investors for development risk while offering material upside if execution meets or exceeds base case assumptions.

Take-Two Stock Analysis: Negative Earnings Mask Strong Balance Sheet Fundamentals

Take-Two’s income statement currently reflects peak investment spending, with operating margins of -59.34% in Q3 FY2026 and negative return on invested capital. However, balance sheet strength provides substantial financial flexibility heading into the commercial harvest phase.

The company maintains approximately $2 billion in cash reserves against a debt-to-equity ratio of 0.88, creating ample liquidity to weather any launch timing volatility. More importantly, operating cash flow conversion improved dramatically to 300.51% in Q3, signaling that the business is approaching the inflection point where development cash burn transitions to margin expansion.

Management guided fiscal 2026 net bookings to $5.9-6.0 billion, representing modest sequential growth before GTA VI’s expected transformational impact in fiscal 2027. The company’s ability to sustain $6 billion in annual bookings without its flagship franchise demonstrates portfolio resilience from NBA 2K, Zynga mobile titles, and catalog sales.

The GTA VI Valuation Variable: $3-8 Billion Revenue Range Creates Binary Outcomes

Revenue projections for GTA VI span an unusually wide range, creating the primary valuation uncertainty. Conservative estimates from DFC Intelligence project $3 billion in first-year sales, while aggressive forecasts from Konvoy Ventures model $7.6 billion within the first 60 days, including $2 billion on launch day.

The bull case anchors to several favorable precedents. GTA V has sold over 210 million units since 2013, generating an estimated $8-10 billion in lifetime revenue. The install base for PlayStation 5 and Xbox Series X|S has reached approximately 95 million consoles combined, comparable to the installed base when GTA V launched in 2013. Critically, recurrent consumer spending already represents 78% of Take-Two’s net bookings, suggesting strong potential for GTA Online 2 monetization.

The bear case emphasizes execution risk around a potential $100 price point, multiplayer stability at launch, and cannibalization risk from free-to-play competitors like Fortnite and Roblox. Rising hardware costs, escalating prices in other economic sectors, and increasing popularity of free-to-play games could shake up the industry.

At current valuation, investors are implicitly pricing in base case outcomes of $5-6 billion in GTA VI revenue. Any material outperformance creates asymmetric upside, while underperformance relative to conservative $3 billion estimates would likely trigger 20-30% downside to the $140-160 range.

Institutional Ownership Patterns: Smart Money Reducing Exposure Pre-Launch

Institutional ownership structure reveals cautious positioning despite bullish public commentary. Total institutional ownership stands at approximately 90.86%, with Vanguard Group, BlackRock, and Saudi Arabia’s Public Investment Fund holding the largest positions.

However, Vanguard trimmed its position by 2.6%, selling 294,232 shares in recent quarters, while multiple directors and C-suite executives executed significant sales. CEO Strauss Zelnick sold 65,000 shares worth $15 million over six months with zero offsetting purchases, alongside material transactions from the CFO, President, and Chief Legal Officer.

This selling pattern doesn’t necessarily signal lack of conviction in the business, as executives regularly monetize equity compensation for diversification purposes. However, the complete absence of insider buying seven months before the industry’s largest launch creates optics that sophisticated investors should monitor. When management has visibility into development milestones, marketing reception, and pre-order dynamics, their trading activity provides potentially informative signals beyond standard SEC disclosures.

Margin Expansion Thesis: Path to 25-30% EBITDA Margins Post-GTA VI

The investment thesis ultimately hinges on Take-Two’s ability to normalize margins following GTA VI’s launch. Profitable video game publishers typically generate EBITDA margins of 25-35%. Electronic Arts, for reference, maintains EBITDA margins around 28%, while Activision historically operated at 30-35% before the Microsoft acquisition.

Analysts project 60% year-over-year earnings growth as the company emerges from its heavy investment cycle, with fiscal 2027 EPS projected at $7.79, representing a 103.6% increase from $3.83. If Take-Two achieves $8 billion in FY2027 revenue with 28% EBITDA margins, the business would generate approximately $2.24 billion in EBITDA, justifying current enterprise value at roughly 17x EBITDA, a premium but defensible multiple given growth durability from GTA Online’s expected 5-10 year monetization runway.

The margin expansion case depends on several execution variables: successful transition of development resources to post-launch content creation, effective monetization of GTA+ subscription services, and operating leverage from Zynga’s integration. Any meaningful margin disappointment would compress valuation multiples and trigger downgrades across the analyst community.

Technical Support Levels and Entry Point Optimization

From a technical perspective, TTWO has established key support near the $187-190 zone, representing the 52-week low. The stock’s 200-day moving average sits at approximately $220, with the current $197.50 price trading 10% below this intermediate-term trend line.

Volume patterns show no signs of capitulation despite the 25% drawdown, with average daily volume of 2.02 million shares remaining consistent with historical ranges. This suggests the decline reflects gradual de-risking rather than forced liquidation or fundamental deterioration.

For investors establishing positions, a disciplined entry strategy might involve deploying 40-50% of intended capital at current levels ($195-200), holding 25-30% in reserve for potential tests of $180-185 support, and allocating the final 20-25% after Q4 FY2026 earnings (expected May 2026) when management will provide official FY2027 guidance.

Risk/Reward Assessment: Asymmetric Opportunity for Risk-Tolerant Investors

The risk/reward profile at $197.50 offers compelling asymmetry for investors with appropriate time horizons and risk tolerance. Downside scenarios center on execution failures (technical issues, review scores below 85 Metacritic, multiplayer instability) or exogenous shocks (recession reducing discretionary spending, regulatory intervention on monetization, competitive disruption from AI-generated content).

In catastrophic scenarios where GTA VI generates only $2-3 billion and management fails to execute on margin normalization, the stock could trade down to $130-150, representing 26-34% downside. However, this requires both revenue underperformance AND margin disappointment simultaneously occurring.

Conversely, base case execution with $6-7 billion in GTA VI revenue and successful margin expansion supports $270-290 targets (+37% to +47% upside). Bull case scenarios where the game generates $8-10 billion and establishes a decade-long live-service revenue stream could drive valuations to $350-400 (+77% to +103%).

The expected value calculation therefore favors long exposure, particularly for investors who can maintain positions through launch volatility and focus on 18-24 month outcomes rather than quarterly fluctuations.

Conclusion: Fairly Priced on Base Case Assumptions, Attractive on Disciplined Entry

After comprehensive analysis of valuation multiples, analyst consensus, financial health, institutional positioning, and risk/reward dynamics, Take-Two Interactive appears fairly to moderately undervalued at current levels assuming base case commercial outcomes.

The stock trades at approximately 6.4x fiscal 2027 estimated revenue and offers 40% upside to consensus price targets with a strong buy rating from 93% of covering analysts. While the $9 billion development investment creates temporary margin compression and negative trailing earnings, the balance sheet remains robust and cash flow metrics suggest approaching inflection.

For investors willing to accept execution risk on the industry’s most anticipated entertainment product, current share price weakness presents a reasonable entry point with asymmetric risk/reward favoring the long side. The optimal approach involves building positions gradually, maintaining strict position sizing discipline (3-5% of portfolio), and establishing clear exit parameters if development delays or launch quality issues emerge.

The critical catalysts to monitor include: Q4 FY2026 earnings (May 2026) when management will formalize FY2027 guidance, pre-order metrics and marketing reception through summer 2026, and November 19, 2026 launch day sales data. Investors who can navigate this timeline while maintaining conviction through volatility may find Take-Two at $197.50 represents one of the decade’s most compelling risk/reward opportunities in interactive entertainment.

—

Disclaimer: This Take-Two stock analysis is for informational purposes only and does not constitute financial advice. Investors should conduct their own due diligence and consult licensed financial advisors before making investment decisions.

I agree, the GTA VI hype is definitely a big factor influencing investor sentiment around TTWO right now.