Bloomberg’s April 2025 bombshell on EA Layoffs in guide of latest restructuring looked like another gaming industry bad-news day. In hindsight, it was the final chapter of acquisition engineering — and the most financially revealing one yet.

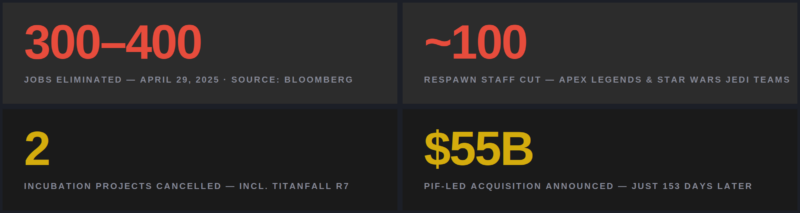

On April 29, 2025, Bloomberg’s Jason Schreier broke the story that Electronic Arts was cutting between 300 and 400 employees and cancelling a Titanfall extraction shooter in development at Respawn Entertainment under the codename R7.

The announcement read like a familiar gaming industry headline: another studio, another round of cuts, another beloved franchise shelved. But the EA layoffs and Titanfall cancellation were not a routine restructuring. They were the closing move in a deal sequence that would culminate just five months later in the largest leveraged gaming buyout ever recorded — Saudi Arabia’s Public Investment Fund acquiring EA for $55 billion.

What Bloomberg Actually Reported

The specifics matter. Bloomberg reported that between 300 and 400 positions were eliminated across EA, with approximately one-third — around 100 roles — coming from Respawn Entertainment, the studio behind Apex Legends and the Star Wars Jedi franchise. The cuts directly impacted teams working on both live titles, as well as two cancelled incubation projects.

Respawn confirmed it was stepping away from “two early-stage incubation projects” and making “targeted team adjustments” across Apex Legends and Star Wars Jedi. PC Gamer confirmed the cancelled projects included the Titanfall extraction shooter codenamed R7 and a second multiplayer FPS shelved earlier in 2025.

EA’s official response was a masterclass in corporate language designed to say nothing: “As part of our continued focus on our long-term strategic priorities, we’ve made select changes within our organization that more effectively aligns teams and allocates resources in service of driving future growth.” Parsing that sentence with a financial eye reveals exactly what was happening.

The EA Layoffs Pattern That Precedes Every Major LBO

Private equity and sovereign wealth fund acquisitions — particularly leveraged buyouts — follow a recognisable financial grammar. Before a deal closes, the target company’s balance sheet is made as clean as possible. Non-core assets are shed. Headcount is rationalised. Free cash flow is maximised. Projects with uncertain return profiles are cancelled. The company, in short, is made to look like the best version of itself on paper — because that paper is what a buyer prices off.

Now read EA’s April 2025 restructuring through that lens. The Titanfall R7 project was an extraction shooter — a genre that had just watched Bungie’s Marathon struggle and the broader extraction market saturate. Its expected development cost would have been tens of millions with no guaranteed revenue. Cancelling it removes a forward liability from the books. The second cancelled project was at an even earlier stage. Both were “incubation” — pre-revenue, pre-production scale, pure cash burn. Cutting them was not a creative failure. It was a financial decision.

The Respawn cuts to Apex Legends and Star Wars Jedi teams are more pointed. These are EA’s highest-profile owned live-service franchises — the exact assets PIF was buying EA for. Leaning those teams down reduces ongoing operating costs on the very properties that would be used to service the $20 billion in acquisition debt post-close.

“Every cancelled project was a forward liability removed from the books. Every job cut was free cash flow returned to the acquirer’s debt model. This was not cost discipline — it was acquisition arithmetic.”— Gaming & Finance Desk Analysis

This Was EA’s Second Restructuring in 15 Months

The April 2025 round was not EA’s first. In February 2024, EA cut 670 employees and cancelled the Respawn Star Wars FPS — a project that would have competed directly with Disney’s Epic Games universe deal that had just been announced. At that point, PIF already held close to 9.9% of EA’s stock, having been building the position since 2020.

The full timeline of restructuring activity maps perfectly onto PIF’s acquisition build-up:

| 2020 | PIF enters EA – Begins building stake. Gaming named a Vision 2030 priority sector. |

| Mar 2023 | Round 1 — 774 cuts First major post-pandemic restructuring across EA. |

| Feb 2024 | Round 2 — 670 cuts Star Wars FPS cancelled. PIF stake reaches ~9.9%. |

| Apr 2025 | Round 3 — 300–400 cuts Titanfall R7 cancelled. Bloomberg breaks the story. Five months to close. |

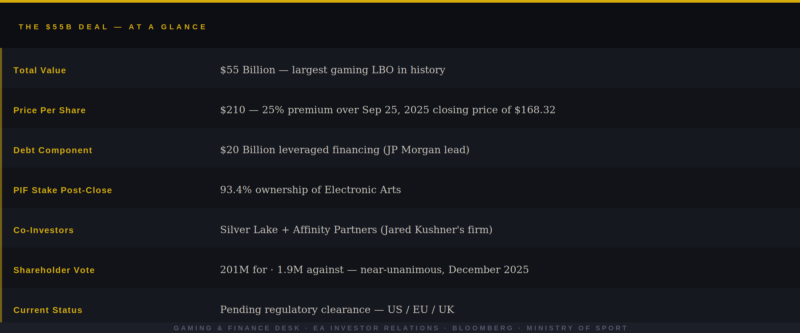

| Sep 2025 | $55B deal announced PIF, Silver Lake & Affinity Partners consortium confirmed at $210/share. |

| Dec 2025 | Shareholders approve 201M votes for. 1.9M against. Awaiting global regulatory clearance. |

Each round of cuts removed more margin drag, more speculative project risk, and more headcount overhead that would complicate a debt-financed takeover. The sequencing is too consistent and too financially coherent to be coincidental.

What Titanfall’s Death Tells Us About PIF’s Real Agenda

Titanfall is one of the most beloved dormant franchises in first-person shooter history. The R7 extraction shooter would have been the first new game in the universe since Titanfall 2 in 2016. Its cancellation — at a moment when Respawn was also absorbing job cuts across its live teams — was met with genuine heartbreak online.

But consider what PIF was actually acquiring EA for. As Luminate’s analysis makes clear, the EA Sports brand with its multiple annual franchise releases was the primary commercial motivator behind the transaction — not new IP bets. EA Sports FC alone generates hundreds of millions in annual revenue through its Ultimate Team live-service model. Madden NFL is similarly recurring and monetised. These are annuity-style cash flows, entirely predictable, and perfect for servicing a leveraged debt stack.

A Titanfall extraction shooter entering a crowded market, built on nostalgia, with uncertain monetisation and a multi-year runway to profitability? That is the exact opposite of what you want on the books when you are about to be acquired for $55 billion and need your franchises to reliably generate cash that services $20 billion in debt every single quarter.

The Debt Load Nobody Is Treating Seriously Enough

Here is the number that should dominate every conversation about this deal but rarely does: $20 billion. That is the leveraged debt component of the $55 billion acquisition, with JP Morgan leading the financing. As PC Gamer noted at the time of shareholder approval, the debt load leaves EA exposed to massive risk — with the only real backstop being the Saudi crown’s appetite for the deal.

To contextualise: EA reported $7.5 billion in revenue in fiscal 2025. Against $20 billion in debt, even at conservative interest rates, the annual debt service obligation could approach $1–1.5 billion depending on terms. Every cancelled project and shed headcount that preceded the deal marginally improved that coverage ratio. This is why the April layoffs read, in retrospect, as final-stage financial housekeeping.

Shareholders Approved. Regulators Remain.

EA shareholders voted overwhelmingly in favour of the acquisition in December 2025 — 201 million votes for versus just 1.9 million against. The deal now sits with global regulators in the US, EU, and UK. Given PIF’s sovereign status and the geopolitical relationships underpinning the consortium, regulatory approval is widely expected, though not guaranteed.

If and when it clears, EA becomes the crown asset of the most ambitious gaming empire assembled outside the traditional industry: PIF’s portfolio already includes significant stakes in Nintendo, Capcom, Take-Two Interactive, and Scopely. EA sits at the top of that stack — the studio that prints sports gaming revenue annually, with a back catalogue reaching into film, franchise gaming, and competitive esports.

What the Affected Workers Deserve to Know

The developers, QA staff, publishing coordinators, and marketing employees who received notices on April 29, 2025, were told their cuts were about “long-term strategic priorities” and “driving future growth.” That language was not technically false. It just omitted the most important part of the strategic context: the growth being prioritised was not EA’s as a public company — it was the acquirer’s return profile on a $55 billion leveraged bet.

The Titanfall game they were building would have been an extraordinary product. It was cancelled not because it lacked ambition or commercial potential, but because a speculative new franchise does not fit the financial model of a company being valued primarily on its annuity sports franchises and prepared for the largest take-private transaction in gaming history.

The EA layoffs and Titanfall cancellation were the final act. The curtain had been falling since 2020, when PIF started buying shares. Most people in the industry just did not know which play they were watching.