Square Enix reported declining sales in its most recent earnings but the company does seem to be gearing up for 2026 and might end up becoming one of the best performing stocks of 2026.

Exchange: Tokyo

Stock Code: TYO:9684

Market Cap: 1.03 Trillion Japanese Yen

Square Enix Reports Declining Sales

For the nine months ended Dec. 31, 2025, Square Enix reported net sales of 215.4 billion yen, down by 13.3%. meanwhile, the company’s profit was up 3.6% to 25.6 billion yen.

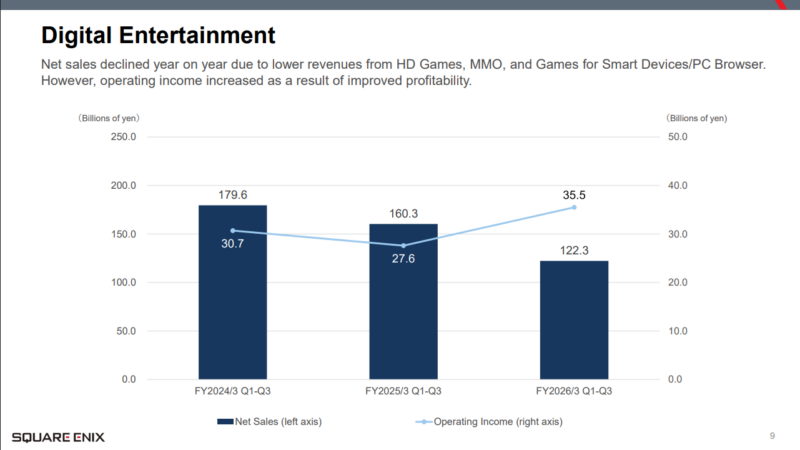

However, what really stands out in the most recent earnings is that the game developer booked a 23.7% decline in its digital entertainment net sales of around 112.3 billion yen. The decline in net sales was linked to lack of revenue from new titles.

However, the company’s catalog titles did well, adding to a 39% increase in the company’s operating income.

Net sales were also down for smart devices and PC browser sub-segment due to “weakness in existing titles.”

New Games to Turn the Tide?

The company announced PARANORMASIGHT: The Mermaid’s Curse, the second coming in the series following the success of PARANORMASIGHT: The Seven Mysteries of Honjo. The game will be coming to Nintendo Switch and other major platforms.

Meanwhile, Final Fantasy VII remake series will be launched on June 3.

These two titles are expected to boost net sales through 2026 and could have a big say on how the company’s earnings per share look like by the end of 2026.

As of Dec. 31, 2025, the company decreased its liabilities by 931 million yen, due to various factors such as decreased asset retirement obligations and provision for office relocation.

However, the company has raised its full-year profit forecasts for the fiscal year ending March 31 and has kept net sales guidance unchanged at 280 billion yen.

Square Enix Buy or Sell?

With a 90% probability hold a price between $14.1 and $17.78, there are mixed signals at the moment. The latest Final Fantasy XIV expansion and exclusivity with PlayStation could limit sales.

The company trades on a P/E of 38.7x, which is well above the JP Entertainment industry average of 19.8x and peer average of 21.9x, which is a valuation risk, especially if expectations cool.