By Taimoor Khan | March 25, 2026 | PressPlay Finance

GameStop Corp. (NYSE: GME) delivered its Q4 FY2025 earnings on March 24, 2026 — and the headline number told only half the story of GameStop Q4 FY2025 Earnings Analysis.

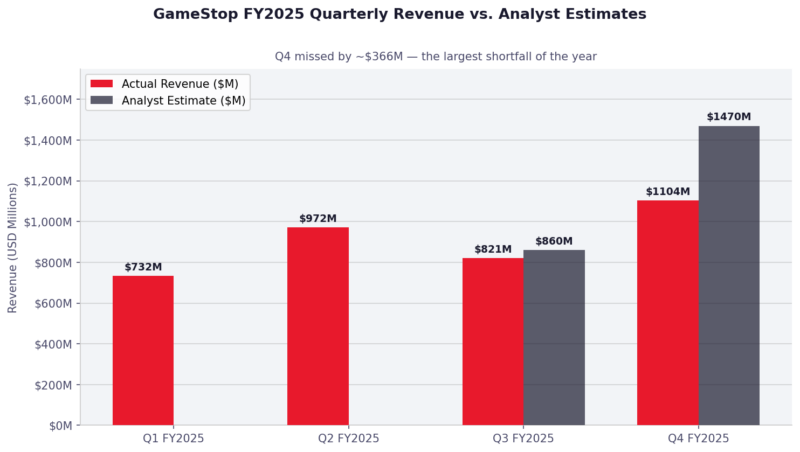

The company beat earnings-per-share (EPS) forecasts convincingly, posting adjusted EPS of $0.49 against a Wall Street consensus of $0.37. But revenue? A completely different picture. Q4 revenue came in at $1.10 billion — a 13.9% year-over-year decline and a $366 million miss against the $1.47 billion analyst estimate. In GameStop’s most important quarter of the year, its holiday quarter, the top line collapsed. GME stock fell approximately 6.5% in after-hours trading, closing the next session around $21.30 from a pre-earnings close of $22.81.

This is a GameStop Q4 FY2025 earnings analysis that cuts through the noise. We examine the revenue miss, the profitability paradox, the category-by-category breakdown, Ryan Cohen’s deafening M&A silence, and what GME stock performance tells us about investor sentiment in 2026.

Q4 FY2025 At A Glance: Key Financial Metrics

| Metric | Q4 FY2025 | Q4 FY2024 | YoY Change |

| Revenue | $1.10B | $1.28B | ▼ 13.9% |

| Analyst Est. | $1.47B | — | MISSED |

| Adj. EPS | $0.49 | $0.30 | ▲ 63% |

| EPS Estimate | $0.37 | — | BEAT |

| Adj. Op. Income | $147.7M | $84.4M | ▲ 75% |

| Net Income | $127.9M | $131.3M | ▼ 2.6% |

| Cash Position | $9.0B | $4.8B | ▲ 87.5% |

| GME Stock (Post) | $21.30 | $22.81 | ▼ 6.6% |

Sources: GameStop Investor Relations | TipRanks Analyst Data | SEC EDGAR Filings

1. The Revenue Miss Is More Alarming Than It Looks

Let’s be direct: missing revenue by $366 million in Q4 — the holiday quarter — is not a rounding error. It’s a structural indictment.

GameStop’s Q4 revenue of $1.10 billion represented a 13.9% year-over-year decline. Context makes this worse: Q3 FY2025 had already seen a 4.6% YoY revenue drop to $821 million. There is no quarter-over-quarter bounce story here. The top line is in secular freefall, and the most commercially important quarter in the retail calendar did nothing to reverse it.

For a publicly listed specialty retailer, two consecutive quarters of revenue decline heading into Q4 — followed by a holiday miss of this magnitude — is exactly the kind of trajectory that strips equity premium fast. Full-year FY2025 revenue came in at $3.63 billion, down from $3.82 billion in FY2024. Over a three-year period, GameStop’s revenue has contracted by more than 22%.

Chart 1: GameStop FY2025 Quarterly Revenue vs. Analyst Estimates — PressPlay Finance

The analyst consensus for Q4 was $1.47 billion — itself a modest expectation. The miss wasn’t a matter of lofty expectations being unmet; it was a business performing materially below even conservative targets during its peak seasonal window.

2. The EPS Beat Is Real — But It’s the Wrong Story

Adjusted EPS of $0.49 vs. a $0.37 estimate sounds like a win. Adjusted operating income of $147.7 million, up from $84.4 million the prior year, sounds like operational progress. So why did GME stock drop? Because this profitability story is 100% a cost-cutting story, not a growth story.

📊 Continue Reading: Gaming Finance Analysis

Deep-dive earnings analysis, M&A coverage, and stock insights for the gaming industry.

SG&A expenses fell to $241.5 million in Q4 from $282.5 million in the prior year period. Full-year SG&A contracted sharply from $1.13 billion to $910 million. That’s nearly $220 million in overhead savings — achieved primarily through store closures, headcount reductions, and the strategic exit from international markets including Canada and France.

This matters enormously from a financial analysis perspective. When EPS beats are driven entirely by cost reduction without commensurate revenue growth, markets correctly treat them with skepticism. You can only shrink so far. Once SG&A is sufficiently lean, there is no more cost lever to pull — and the revenue problem becomes fully exposed.

Full-year FY2025 adjusted net income of $647.4 million versus $131.2 million the prior year is eye-catching, but it includes the benefit of the $2.7 billion convertible note issuance in Q2, interest income on the growing cash pile, and investment gains. Strip those out and the operating business is a much thinner story.

| 📊 DEEP-DIVE ANALYSIS FROM PRESSPLAY FINANCEWant to understand what the GameStop numbers really mean for investors?Read our recently published long-form analysis: GameStop Q4 2025 Earnings Preview — Will Ryan Cohen Deliver?Also explore our full video game finance coverage at PressPlayFinance.com → |

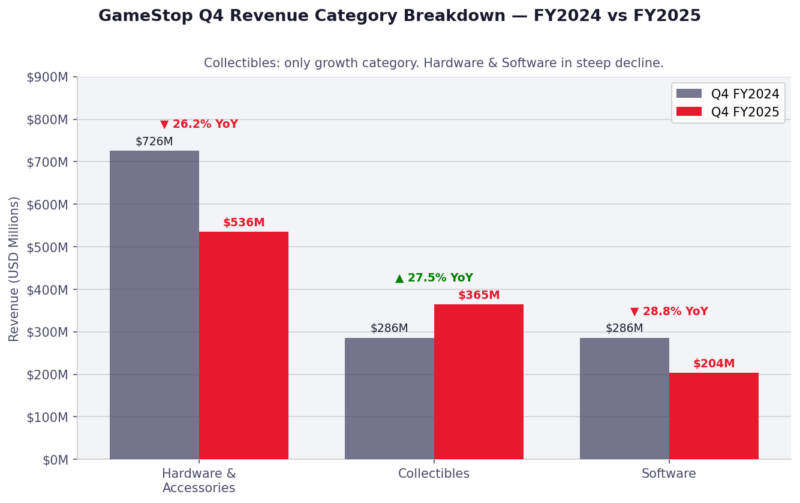

3. Category Breakdown: The Hardware & Software Collapse

The segment-level data is where the real damage becomes visible. Three categories, three very different stories:

- Hardware & Accessories: $535.6M in Q4 FY2025, down from $725.8M in the prior year — a 26.2% decline.

- Software: $203.7M vs. $286.2M prior year — a 28.8% decline. Software is now less than 18.5% of total revenue.

- Collectibles: $365.0M — 33.1% of total revenue. The only category showing forward momentum.

Chart 2: Q4 Revenue Category Breakdown — FY2024 vs FY2025 | PressPlay Finance

Hardware and software — the historical twin pillars of the GameStop business model — are collapsing simultaneously. This is not a cyclical problem caused by a weak console lineup. It is a structural problem driven by digital distribution. According to NPD Group data, physical game sales declined 22% in 2025, while digital downloads and subscription services captured approximately 78% of total game spending.

Collectibles — Funko Pops, trading cards, retro gaming merchandise, high-end fan culture products — is Cohen’s strategic response to this structural shift. The margins are genuinely better, and the category grew 27.5% year-over-year. But at $365 million, it cannot offset the combined $373 million decline in hardware and software. It’s a lifeboat, not a new ship.

4. GameStop Q4 FY2025 Earnings Analysis: YTD Trajectory & Post-Earnings Drop

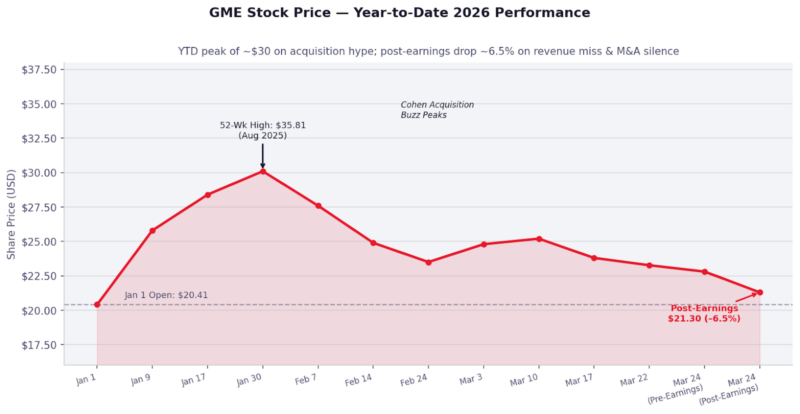

GameStop stock entered 2026 at approximately $20.41. Through January and into early February, shares surged to a YTD peak in the $28–30 range, driven almost entirely by Ryan Cohen’s January CNBC interview in which he described pursuing a “very, very, very big” acquisition of a publicly traded consumer company. That narrative — not operating fundamentals — was the price catalyst.

Chart 3: GME Stock YTD Price Performance 2026 — Peak of ~$30 to Post-Earnings ~$21.30 | PressPlay Finance

From that peak, shares drifted lower through February and March as acquisition specifics failed to materialize. By earnings day, GME had pulled back to approximately $22.81 — representing a meaningful discount from the YTD peak but still a ~14% YTD gain on a price-to-narrative basis.

Post-earnings, shares dropped approximately 6.5% to around $21.30 in extended trading. The 52-week range sits between $19.93 and $35.81, suggesting the market views $20 as a rough floor — consistent with the approximate net cash per share value. The Cohen premium, once worth $15+ above the cash floor, has compressed significantly as M&A clarity remains absent.

At the current ~28x P/E ratio, GameStop trades at a meaningful premium to specialty retail peers, which typically trade at 15–20x earnings. That premium is entirely justified by — and contingent on — a transformative M&A announcement. Without it, the fundamental case for the stock above its cash value weakens materially.

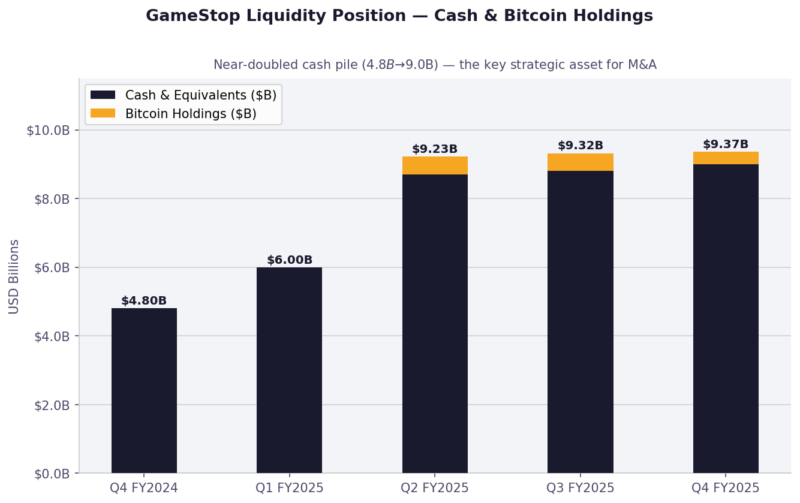

5. The $9 Billion War Chest: Asset or Liability?

The single most compelling number in this earnings report is not revenue or EPS. It’s the cash position: $9.0 billion in liquid assets and equivalents, up from $4.8 billion a year ago — an 87.5% increase. Add $368.4 million in Bitcoin holdings, and GameStop’s total liquidity stack approaches $9.4 billion.

Chart 4: GameStop Cash Position & Bitcoin Holdings — Q4 FY2024 to Q4 FY2025 | PressPlay Finance

To understand how significant this is: GameStop’s total market capitalization is approximately $10 billion. Net cash per share sits around $19.50. You are essentially buying the operating retail business for roughly $1–2 per share above the cash floor. In one sense, this provides meaningful downside protection.

But idle cash is not value creation. For a publicly listed company, cash on the balance sheet earns interest income — and GameStop is benefiting from that in its income statement. But it does not justify a significant market premium unless management can deploy it productively. $9 billion sitting in Treasuries, while the core business contracts at 13.9% per quarter, is not a business strategy.

Cohen’s compensation structure makes the deployment pressure existential: his options only vest if GameStop reaches a $100 billion market capitalization while achieving $10 billion in cumulative EBITDA. There is zero path to those numbers through organic retail operations. The acquisition is not optional — it’s structurally necessary for management incentives to pay out.

6. The Acquisition Silence: The Market’s Real Disappointment

Of everything in this GameStop Q4 FY2025 Earnings Analysis, the absence of acquisition news was the most damaging development for GME stock.

Investors had built significant expectation — and premium — into the stock price based on Cohen’s own rhetoric. In January 2026, he told CNBC that GameStop was pursuing a deal he described as “way more compelling than Bitcoin.” He characterized the potential acquisition as either “genius or totally foolish” — language that signals an audacious, large-scale move is being contemplated.

The conference call delivered nothing. No timeline. No industry focus. No indication that the deal pipeline is progressing. For a company sitting on $9 billion in cash and actively building a narrative around transformative M&A, that silence is not neutral — it’s a negative signal.

Three possibilities explain the silence, none of them particularly bullish in the short term:

- The deal fell through: Negotiations collapsed or a target rejected Cohen’s approach. This would explain the lack of disclosure.

- Regulatory or disclosure constraints: Active deal discussions may prevent public disclosure under SEC rules — a potentially bullish reading.

- Strategic patience: Cohen may be waiting for macro volatility to drive down target valuations before striking. Disciplined, but markets are impatient.

The Wall Street consensus price target remains $13.50 with a “Reduce” rating — implying approximately 37% downside from current levels. That consensus reflects what analysts believe GME is worth as a pure retail business, stripped of the Cohen optionality premium. The gap between $13.50 and $21+ is entirely Ryan Cohen’s acquisition narrative.

7. Key Risk Factors for GME Stock Investors

- Structural revenue decline: Physical gaming is a shrinking market. Without M&A diversification, revenue will continue contracting regardless of cost efficiency.

- Acquisition execution risk: A bad deal at an overvalued price could permanently impair the $9B war chest and destroy shareholder value.

- Bitcoin concentration: $368M in BTC introduces crypto volatility into an already unpredictable balance sheet.

- Meme premium compression: GME trades on narrative. If Cohen’s M&A story fades, the premium above cash value could evaporate rapidly.

- No forward guidance: GameStop does not provide formal guidance, meaning investors are flying blind on both operational and strategic direction.

8. Three Post-Earnings Scenarios for GME

Bull Case ($27–$30)

Cohen announces a credible acquisition within 60 days. Collectibles continues double-digit growth. Bitcoin appreciates. M&A target operates in a higher-margin, higher-growth sector that justifies the premium.

Base Case ($19–$23)

Revenue decline continues at mid-single digits. Cost cuts sustain profitability. Acquisition timeline remains vague through H1 2026. Stock consolidates near its cash floor with high volatility.

Bear Case ($13–$17)

Acquisition deal either never materializes or destroys value when announced. Revenue accelerates downward. Bitcoin drops 50%+. Cohen premium evaporates and stock re-rates toward analyst consensus of $13.50.

Final Take: A Capital Allocation Vehicle With a Shrinking Core

GameStop is no longer a video game retailer in any meaningful strategic sense. It is a capital allocation vehicle — $9 billion in search of a transformative deal — with a declining retail operation attached to it. The EPS beat is a testament to Ryan Cohen’s cost discipline. The revenue miss is a testament to the structural reality of the physical gaming market in 2026.

For investors in GME stock, the operating business is largely irrelevant to the investment thesis. What matters is: (1) Cohen’s ability to identify and execute a transformative acquisition at a reasonable price, (2) the timing of that announcement, and (3) whether the acquired business can realistically support the $100 billion market cap target embedded in Cohen’s compensation structure.

Until that clarity arrives, you are paying a speculation premium on top of a $19.50/share cash floor. That may be a comfortable trade for risk-tolerant investors. For fundamental long-term investors, the absence of M&A clarity after months of public rhetoric is a credibility risk that shouldn’t be dismissed.

The holiday quarter revenue miss in a structurally declining business, with no acquisition news and no forward guidance, is not a thesis-confirming report. It is a thesis-challenging one.

ABOUT THE AUTHOR

Taimoor Khan is a financial analyst covering publicly listed video game developers and interactive entertainment companies for PressPlay Finance. His coverage focuses on the intersection of consumer gaming trends and equity markets. Follow his analysis at pressplayfinance.com.

DISCLAIMER

This article is for informational purposes only and does not constitute investment advice. All data is sourced from publicly available filings and analyst reports. PressPlay Finance does not hold positions in securities mentioned. Past performance is not indicative of future results. Readers should conduct their own due diligence before making investment decisions.