How an aggressive M&A strategy, mobile market disruption, and strategic missteps turned a Sega Sammy, a gaming powerhouse, into a cautionary tale of corporate overreach

In what industry analysts are calling one of the most dramatic reversals in Japanese gaming history, SEGA SAMMY Holdings announced on February 13, 2026, that it is projected to book a net loss of ¥13 billion for the fiscal year—a stunning ¥50.5 billion swing from its initial profit forecast of ¥37.5 billion.

The answer lies in a perfect storm of failed acquisitions, market disruption, and strategic miscalculation that converged in the company’s third quarter, exposing fundamental weaknesses in both its M&A approach and core business operations. At the heart of the crisis: ¥46.3 billion in impairment charges on two recent acquisitions that were supposed to fuel the company’s next chapter of growth.

The Rovio Gamble: A ¥101 Billion Bet Gone Wrong

In August 2023, SEGA SAMMY made what seemed like a logical move: acquire Rovio Entertainment, the Finnish creator of Angry Birds, for approximately ¥101.8 billion. The strategic rationale was compelling—gain mobile gaming expertise, acquire the beloved Angry Birds IP, and obtain Rovio’s proprietary Beacon technology for optimizing free-to-play games.

But timing, as they say in the gaming industry, is everything. And SEGA SAMMY’s timing couldn’t have been worse.

“What we couldn’t have fully anticipated was the speed and scale of market consolidation. Within months of the acquisition, the mobile gaming landscape transformed completely.”

Just as SEGA SAMMY was closing the Rovio deal, the mobile gaming market was entering a period of unprecedented consolidation. Monopoly Go, which launched in April 2023—four months before the Rovio acquisition completed—became an instant phenomenon, dominating user acquisition budgets across the industry.

These titles didn’t just compete for players—they fundamentally altered the economics of mobile gaming. User acquisition costs skyrocketed as these well-funded competitors poured billions into marketing. Mid-tier games like Angry Birds 2, which had been Rovio’s cash cow, found themselves squeezed out of the market.

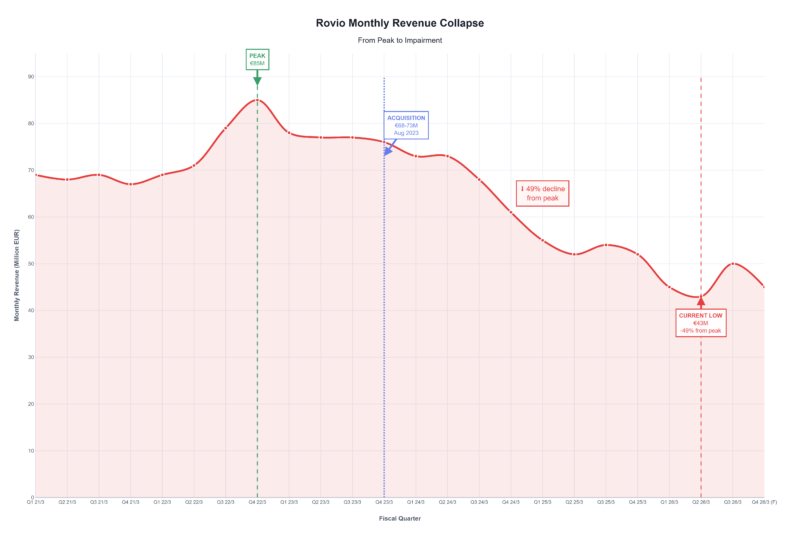

The Rovio Revenue Collapse

Monthly revenue trajectory tells a devastating story:

- Q3 FY2023 (Pre-acquisition peak): €85 million per month

- August 2023 (Acquisition close): €68-73 million per month

- Q3 FY2026 (Current low): €43 million per month

- Total decline: 49% from peak, 41% from acquisition

The problems went beyond market conditions. Rovio’s new game development strategy—focused on creating titles based on new intellectual properties rather than leveraging established franchises—failed spectacularly. Multiple titles missed their KPI targets, faced development delays, or were cancelled entirely.

Most damning of all: the much-anticipated SEGA-Rovio collaboration, Sonic Rumble, launched in November 2025 to disappointing results. Customer acquisition fell significantly below expectations, and all key performance indicators—retention, monetization, daily active users—underperformed.

In December 2025, SEGA SAMMY management made the painful decision: recognize a ¥31.3 billion impairment on Rovio’s goodwill. Nearly one-third of the acquisition price, written off less than two and a half years after the deal closed.

Stakelogic: When Regulation Strikes

If the Rovio acquisition was a case of bad timing, the Stakelogic deal was a masterclass in regulatory risk underestimation.

SEGA SAMMY acquired Netherlands-based Stakelogic B.V. in October 2025 for approximately ¥21.3 billion, seeing it as a strategic entry point into the European online gaming and iGaming markets.

There was just one problem: between the acquisition announcement and completion, the Netherlands—Stakelogic’s primary market—implemented significantly stricter gambling regulations.

“The regulatory environment fundamentally changed during the acquisition process,” explained one industry analyst familiar with the deal. “The Dutch market, which was supposed to be Stakelogic’s foundation, essentially contracted overnight. And there was no contingency plan.”

The company now expects to recognize an additional ¥15 billion impairment on Stakelogic at the fiscal year-end—representing approximately 70% of the purchase price. Combined with the Rovio impairment, SEGA SAMMY will have written off ¥46.3 billion in goodwill in a single fiscal year.

To put that in perspective: ¥46.3 billion is equivalent to nearly 14% of the company’s total equity, gone in a matter of months.

The Core Business Crisis Hidden in Plain Sight

While the acquisition impairments dominated headlines, they masked an equally serious problem: SEGA SAMMY’s core Entertainment Contents business was struggling.

The Consumer business, centered on packaged game sales and free-to-play titles, missed its forecast by ¥9 billion. Full game sales came in at ¥72.1 billion versus an initial forecast of ¥78.1 billion. Even more concerning, catalog sales—revenue from older titles—declined 12.8% versus expectations.

“We’re seeing structural issues in how we approach digital distribution, customer lifetime value optimization, and data-driven decision making. We’re frankly behind the curve.”

Internal reviews identified multiple structural problems:

- Digital Transformation Lag: SEGA’s approaches to lifetime value maximization and recurring revenue models remained underdeveloped

- Geographic Fragmentation: Regional publishing offices operated independently, preventing global simultaneous launches

- Marketing Obsolescence: Customer acquisition costs rising while return on investment fell

- Quality Control Issues: Football Manager 26 launched with significant bugs requiring extensive post-launch updates

One bright spot emerged: the Pachislot and Pachinko Machines business exceeded revised expectations, driven by hit titles like Smart Pachislot Bakemonogatari. But even this success was muted—operating income still declined 47.9% year-over-year.

The Cash Crunch: When Financial Flexibility Evaporates

Perhaps the most concerning aspect of SEGA SAMMY’s crisis isn’t the impairments themselves—it’s how they’ve eroded the company’s financial flexibility exactly when it needs it most.

Cash and deposits plummeted from ¥200.3 billion in March 2025 to ¥142.9 billion by December 2025. The company’s net cash position swung from positive ¥49.3 billion to negative ¥2.3 billion.

This cash crisis forced a dramatic reversal in capital allocation strategy. Strategic M&A allocation was slashed from ¥80+ billion to ¥20 billion, and large-scale M&A was suspended indefinitely.

“They’re in a difficult position. Shareholders want returns, but the company desperately needs that cash to fix its operational problems and invest in its core business transformation.”

Anatomy of a Strategic Failure

How did a company with SEGA SAMMY’s pedigree—home to iconic franchises like Sonic, Yakuza, Persona, and Total War—end up in such dire straits?

At each decision point, SEGA SAMMY made choices that seemed reasonable in isolation but proved disastrous in combination. The company pursued growth through acquisitions while its core business needed strengthening. It allocated capital aggressively based on optimistic cash flow projections that never materialized. It underestimated regulatory risks and market disruption risks simultaneously.

Most fundamentally, it attempted to transform into a data-driven, digitally-native gaming company by buying capabilities rather than building them organically—only to discover that organizational cultures, technologies, and business models don’t integrate as easily as PowerPoint presentations suggest.

The Road Ahead: Can SEGA SAMMY Recover?

Despite the dire headlines, SEGA SAMMY’s situation isn’t hopeless. The company retains valuable assets: beloved IP franchises, a strong position in Japan’s Pachislot and Pachinko markets, growing licensing revenue (up to ¥12.2 billion through Q3), and a still-healthy equity ratio of 56.2%.

Recovery Initiatives

- Rovio Restructuring: Appointed Daniel Svärd (formerly of King/Candy Crush) as COO; refocusing on Angry Birds and SEGA IPs; targeting 30% external payment rate within five years

- Consumer Business Transformation: Establishing dedicated data analytics organization; redesigning KPIs and marketing criteria; strengthening global publishing coordination

- Gaming Business Consolidation: Restructuring Stakelogic; converting content for online/social casino use; advancing U.S. market entry

- Capital Discipline: Large-scale M&A suspended; focus on organic growth; ¥20B share buyback program

- Transmedia Expansion: Leveraging Angry Birds Movie 3 (December 2026) and Sonic 4 (March 2027) for IP growth

Lessons for the Gaming Industry

SEGA SAMMY’s crisis offers valuable lessons that extend far beyond one company’s struggles:

1. Timing is Everything in Tech M&A: The Rovio acquisition happened at precisely the wrong moment in the mobile gaming cycle. Even with perfect execution, market timing can make or break a deal.

2. Regulatory Risk is Real: The Stakelogic impairment demonstrates that regulatory changes can destroy acquisition value faster than any operational issue.

3. Synergies Must Be Validated, Not Assumed: Beacon technology was supposed to boost SEGA’s titles. Sonic Rumble was supposed to prove collaboration value. Neither delivered.

4. You Can’t Buy Digital Transformation: SEGA SAMMY tried to acquire capabilities rather than building them organically. The approach failed because digital transformation requires cultural change.

5. Cash is King During Crisis: Cash depletion at exactly the moment maximum flexibility was needed demonstrates why conservative balance sheets matter.

“The fundamental error was attempting growth through acquisition while the core business needed strengthening. It created a dual burden that proved unsustainable.”

Conclusion: A Cautionary Tale

SEGA SAMMY’s ¥46.3 billion impairment crisis represents more than accounting writedowns. It’s a story about the perils of overconfident growth strategies, the dangers of inadequate due diligence, and the compounding effects of strategic errors.

The company that created Sonic the Hedgehog—a character built on speed and momentum—discovered that in corporate strategy, moving fast can be as dangerous as moving slow. Racing toward growth through aggressive M&A while core businesses struggled created a perfect storm of simultaneous crises.

Whether SEGA SAMMY can recover remains an open question. The company has the assets, the IP, and now—painfully—the lessons learned. What it lacks is time and financial flexibility. The next 12-18 months will determine whether this crisis was a temporary setback or the beginning of a longer decline.

For the rest of the gaming industry, SEGA SAMMY’s struggles serve as a stark reminder: in an industry defined by hits and misses, even the biggest names aren’t immune to the consequences of strategic miscalculation. Sometimes the biggest risk isn’t standing still—it’s moving in the wrong direction at full speed.