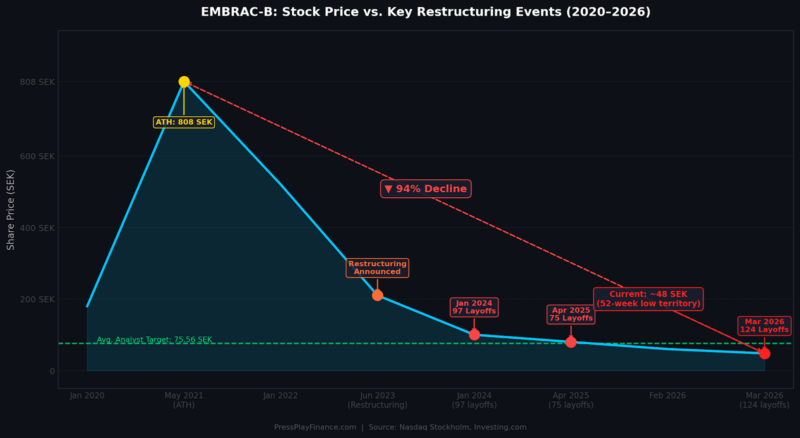

On March 31, 2026, Eidos Montreal confirmed the elimination of 124 employees — its third round of cuts since January 2024. The head of studio, David Anfossi, who spent nearly two decades at the company, also departed. For investors tracking Embracer Group stock on the Nasdaq Stockholm exchange (EMBRAC-B), this event is not a standalone headline. It is the latest data point in a structural narrative that has erased approximately 94% of the company’s peak equity value since its all-time high of 808 SEK in May 2021.

Today, Embracer Group stock trades near 48 SEK — deep in 52-week-low territory — with a market consensus that remains stubbornly optimistic in the face of relentless operational deterioration.

Embracer Group Stock Price vs. Key Restructuring Events (2020–2026)

Source: Nasdaq Stockholm, Investing.com | PressPlayFinance.com

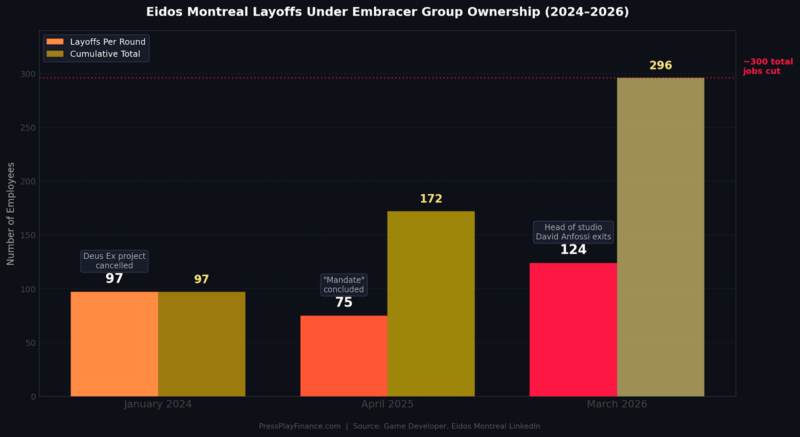

The Eidos Montreal Layoff Timeline: ~300 Jobs Cut in Two Years

The Eidos Montreal acquisition from Square Enix in 2022 — which also included Crystal Dynamics and the Tomb Raider IP — was meant to be a marquee moment for Embracer’s content library. Instead, the studio has become a symbol of the group’s post-acquisition dysfunction.

The cuts have followed a consistent rhythm: January 2024 saw 97 roles eliminated alongside the cancellation of an unannounced Deus Ex project. April 2025 brought a further 75 redundancies, framed by management as the conclusion of a development “mandate.” And now, in March 2026, 124 more employees are gone — along with the institutional memory represented by Anfossi’s exit after 19 years.

Embracer Group stock declined through each of these events, tracking a broader loss of investor confidence in the group’s ability to convert its acquired IP portfolio into a sustainable earnings stream. Each layoff round has been positioned as a cost-efficiency measure — yet the cumulative headcount reduction at a single studio of this calibre raises a more fundamental question: what pipeline remains to justify a re-rating?

Eidos Montreal Layoffs Under Embracer Ownership (2024–2026)

Source: Game Developer, Eidos Montreal LinkedIn | PressPlayFinance.com

What the Stock Tells Us: A 94% Decline Is Not Just a Macro Story

It would be convenient to attribute the collapse of Embracer Group stock entirely to the broader rising-rate environment that pressured leveraged growth companies across 2022–2023. And rates did matter. Embracer’s aggressive M&A strategy — funded largely through debt at near-zero borrowing costs — became acutely exposed when the global rate cycle turned. The collapse of a key Saudi investment partnership in mid-2023 triggered a comprehensive restructuring that included studio closures, project cancellations, and the kind of recurring layoffs we are still witnessing today.

But the market’s continued punishment of Embracer Group stock — even after significant balance sheet repair — tells you that this is now a company-specific execution story, not just a macro one. The stock’s 52-week range of approximately 43 to 128 SEK, combined with an absence of dividend yield and no buyback programme, gives equity holders very little cushion while they wait for a catalyst. The beta of 0.96 suggests the stock moves largely in line with the broader market — meaning underperformance of this magnitude is almost entirely idiosyncratic.

Analyst Consensus vs. Market Reality: A 62% Upside Gap Nobody Believes

The sell-side consensus on Embracer Group stock presents a striking paradox. Based on coverage from nine analysts, the average 12-month price target sits at approximately 75.56 SEK — implying around 62% upside from current levels, with five buy ratings and zero sell recommendations. Yet the stock continues to drift toward its 52-week floor.

This is what the market calls a credibility gap. Bull case models depend on Embracer’s AAA pipeline delivering on schedule — management has guided for 10 AAA releases over the next three fiscal years — and on the net cash position of approximately SEK 5 billion (built through asset divestments including the sale of Easybrain) translating into either a strategic acquisition or a return-of-capital event that re-engages institutional holders.

The bear case, which current Embracer Group stock pricing implicitly endorses, is that recurring studio-level instability — Eidos Montreal being Exhibit A — will erode the very pipeline those price targets are built on. When you cut the same studio three times in two years and lose its founding leadership, you are not just trimming costs. You are also eliminating the creative continuity and institutional IP knowledge that makes a game studio’s future output predictable.

The Cost-Cut Trap: When Restructuring Becomes the Business Model

There is a well-documented risk in distressed media and gaming companies that operational restructuring becomes self-defeating. Embracer Group stock‘s EBITDA margin has improved — running at approximately 20% on a trailing basis — and last quarter’s EPS of 1.77 SEK beat the consensus estimate of 1.01 SEK by a significant 75%. On paper, the restructuring is working. Cash conversion is improving. The balance sheet is de-risked.

Yet a trailing P/E of approximately 2.57x — extraordinarily cheap for a gaming holding company — is not the market awarding a value premium. It is the market applying a deep discount to the quality and predictability of future earnings. The denominator (earnings) looks acceptable today largely because of cost reduction, not revenue growth. And revenue growth, in a games business, is a function of titles released — which is itself a function of studio headcount and creative stability.

In other words, Embracer is at risk of structurally impaired revenue on the other side of this restructuring unless it can demonstrate a credible pipeline from the studios it has retained. The next AAA release timeline, not the next cost-cutting round, will be the true inflection point for the stock.

Investor Takeaway: Wait for Pipeline Proof, Not Just Balance Sheet Repair

Embracer Group stock at 48 SEK with a 62% analyst upside target is either a deep value opportunity or a value trap — and the Eidos Montreal layoffs do nothing to resolve that ambiguity. The balance sheet is cleaner. The cash position is real. But until Embracer demonstrates that its retained studios are producing AAA-quality games on time and on budget, the market will continue to apply a structural discount to any earnings recovery thesis.

For investors with a 12-to-18-month horizon, the next catalyst to watch is Embracer’s upcoming earnings release on May 20, 2026, where management’s pipeline commentary will carry more weight than any headline cost metric. For the 124 employees departing Eidos Montreal — and the approximately 300 who have left since 2024 — the data points are rather more personal.