HOLD Rating for Public Shareholders | Regulatory Approval Expected Q2 2026 | $20B Debt Load Reshapes Capital Structure

By Taimoor Khan

Published: April 14, 2026Last Updated: April 14, 2026

INVESTMENT SUMMARY

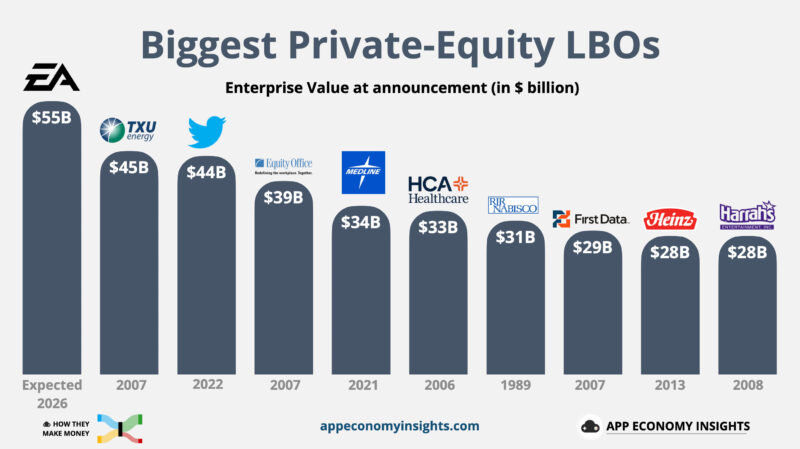

Electronic Arts Inc. (NASDAQ: EA) shareholders approved the company’s $55 billion leveraged buyout by a consortium led by Saudi Arabia’s Public Investment Fund in December 2025, clearing the deal’s only internal hurdle and advancing the transaction to U.S. regulatory review.

The take-private transaction, which is structured at $210 per share in cash, now faces scrutiny from the Committee on Foreign Investment in the United States (CFIUS), with a decision expected by June 2026.

The deal represents the largest leveraged buyout in gaming industry history and positions EA for significant operational changes under PIF’s 93.4% ownership stake.

With $20 billion in debt financing arranged by JPMorgan Chase, the transaction fundamentally alters EA’s capital structure from a zero-debt balance sheet to a leverage profile that will consume approximately 25-28% of current EBITDA for debt service.

RECOMMENDATION: HOLD for public shareholders. Accept tender offer at $210/share upon CFIUS approval. The 3% deal spread versus current trading levels (~$203.79 as of April 10, 2026) does not justify event risk exposure for retail investors.

REGULATORY TIMELINE AND APPROVAL PROBABILITY

The PIF-led consortium announced the acquisition agreement in September 2025, with EA’s board unanimously recommending shareholder approval. Investors approved the transaction on December 22-23, 2025, with the deal now subject to CFIUS review—the federal body responsible for assessing foreign investment national security implications.

Historical precedent suggests CFIUS approval is the base case outcome. According to the Financial Times, multiple sources familiar with the matter indicated the deal is expected to pass regulatory review “easily,” citing the relationship between PIF and the Trump administration. Affinity Partners, which holds a 1.1% stake in the acquisition consortium, is led by Jared Kushner, former senior advisor to President Donald Trump and Trump’s son-in-law.

PIF already maintains a 9.9% stake in EA, which will be rolled over as part of the transaction structure, and holds additional gaming industry investments including positions in Take-Two Interactive Software Inc. (NASDAQ: TTWO), Nintendo Co., Ltd. (TYO: 7974), and Capcom Co., Ltd. (TYO: 9697).

None of these prior investments triggered CFIUS intervention, establishing precedent for Saudi capital deployment in the gaming sector.

The typical CFIUS review timeline ranges from 45 days for initial assessment to 6 months for transactions requiring extended national security analysis. EA and the consortium have indicated an expected close date in the first quarter of the company’s fiscal year 2027, which runs from April 1 through June 30, 2026.

“This transaction represents a significant milestone for EA and our stakeholders,” EA CEO Andrew Wilson stated in the company’s September 2025 announcement. “Under this partnership, EA’s values and commitment to our players, employees, and communities will remain unchanged.”

EA Leveraged Buyout at a Glance

The transaction’s financing structure marks a departure from EA’s historically conservative capital allocation approach. The consortium will acquire 100% of EA’s outstanding shares for $55 billion in cash, funded through $36 billion in equity contributions and $20 billion in debt arranged by JPMorgan Chase.

Post-close ownership will concentrate heavily in PIF, which will control 93.4% of EA’s equity. Private equity firm Silver Lake will hold 5.5%, while Affinity Partners maintains the remaining 1.1%. This ownership concentration differs meaningfully from recent gaming industry consolidation transactions, including Microsoft Corporation’s (NASDAQ: MSFT) $68.7 billion acquisition of Activision Blizzard Inc.—structured as an all-cash strategic acquisition using Microsoft’s balance sheet rather than leveraged financing.

The $20 billion debt load represents approximately 3.5x EA’s estimated fiscal year 2025 EBITDA of $5.7 billion. Assuming a blended interest rate of 7-8% on the debt package, EA will face annual interest expenses of $1.4-1.6 billion—consuming 25-28% of current EBITDA for debt service obligations.

This capital structure shift eliminates EA’s historical financial flexibility. As a public company, EA maintained zero net debt and approximately $6 billion in cash and equivalents as of its most recent quarterly filing. The post-LBO structure prioritizes cash generation for debt service over balance sheet optionality, with meaningful implications for capital allocation toward new intellectual property development, studio acquisitions, and marketing investment.

According to data from PitchBook’s gaming M&A tracker, the EA transaction is part of a broader surge in gaming industry leveraged buyouts during 2025-2026, with first quarter 2026 gaming M&A totaling $7.7 billion across 52 transactions—more than triple the $2.4 billion recorded in Q1 2025.

MARGIN PRESSURE SCENARIOS: COST-CUTTING VS. MONETIZATION INTENSITY

The debt service burden creates pressure for margin expansion through two primary levers: operational cost reduction and revenue optimization via enhanced monetization.

Cost Structure Rationalization

Historical LBO playbooks typically target 15-25% workforce reductions within the first 18 months post-close. EA’s global workforce of approximately 13,000 employees presents opportunity for meaningful expense reduction, though aggressive headcount cuts carry execution risk for franchises requiring sustained development talent.

Assuming a 15-20% workforce reduction (2,000-2,600 employees) at an average fully loaded cost of $150,000 per employee, EA could realize $300-400 million in annual savings. Additional cost reduction opportunities include marketing budget optimization (shift from broad-based brand campaigns to performance marketing), studio consolidation, and general administrative expense rationalization.

A combined cost reduction target of $600 million annually would increase EBITDA margins from the current 76% to approximately 84%, creating additional cushion for debt service coverage. However, this approach risks talent exodus to competitors including Ubisoft Entertainment SA (EPA: UBI), Riot Games, and indie studios—particularly for key franchises like Battlefield (developed by DICE in Stockholm) and Dragon Age/Mass Effect (developed by BioWare in Edmonton).

Revenue Growth via Monetization

The alternative margin expansion path involves increasing revenue per user across EA’s live service portfolio, which generates approximately $4 billion of the company’s $7.5 billion in annual revenue. FIFA/EA Sports FC’s Ultimate Team mode, Apex Legends’ cosmetics and battle pass system, and The Sims’ expansion content represent primary monetization expansion opportunities.

Industry precedent suggests caution on this approach. Activision Blizzard’s 2017 Star Wars Battlefront II loot box controversy generated significant player backlash and regulatory scrutiny across multiple jurisdictions, ultimately forcing monetization model changes. EA itself was at the center of that controversy, highlighting reputational risk from aggressive monetization tactics.

A 10-15% decline in daily active users due to monetization backlash would reduce live service revenue by $400-600 million annually—directly offsetting margin gains and creating debt service coverage risk.

“THE $20 BILLION DEBT LOAD REPRESENTS APPROXIMATELY 3.5X EA’S ESTIMATED FISCAL YEAR 2025 EBITDA OF $5.7 BILLION, CONSUMING 25-28% OF CURRENT EBITDA FOR DEBT SERVICE.”

STRATEGIC RISKS: GEOPOLITICAL EXPOSURE AND FRANCHISE EXECUTION

The transaction introduces geopolitical risk not present in EA’s public company structure. PIF operates as an investment arm of the Saudi Arabian government, led by Crown Prince Mohammed bin Salman, who has faced international scrutiny following the 2018 killing of journalist Jamal Khashoggi.

Consumer advocacy groups have raised concerns about potential cultural influence over EA’s content, particularly for franchises like The Sims (which features LGBTQ+ representation and progressive social themes) and Battlefield (which includes Middle East conflict settings). While CEO Andrew Wilson has stated EA’s values will “remain unchanged,” the 93.4% ownership concentration gives PIF ultimate decision authority over content and creative direction.

From a purely financial perspective, sustained consumer boycotts or brand damage could impact revenue—though historical evidence suggests limited commercial impact from geopolitical controversies in the gaming sector. Saudi Arabia’s ownership of Newcastle United FC (English Premier League) provides a comparable case study, where initial fan protests have diminished without measurable attendance or merchandise revenue decline.

The more immediate franchise execution risk stems from potential talent retention challenges. EA’s premier studios—Respawn Entertainment (Apex Legends), DICE (Battlefield), BioWare (Dragon Age, Mass Effect), and Maxis (The Sims)—operate with significant creative autonomy. An aggressive cost-cutting program or workforce reduction mandate from PIF could trigger departures of senior developers and creative leads, particularly given the competitive market for top-tier gaming talent.

COMPARABLE VALUATION ANALYSIS

The consortium’s $210 per share offer represents a 25% premium to EA’s unaffected closing price of $174.04 on September 26, 2025 (the last trading day before acquisition discussions became public). On an enterprise value basis, the $55 billion purchase price implies an EV/EBITDA multiple of 9.6x based on fiscal 2025 EBITDA estimates.

Comparable gaming publisher valuations as of April 2026:

• Take-Two Interactive (TTWO): 12.5x NTM EBITDA (trading at premium due to Grand Theft Auto VI launch scheduled for November 2026)

• Ubisoft Entertainment (UBI): 7.8x NTM EBITDA (distressed valuation following restructuring announcements)

• CD Projekt S.A. (WSE: CDR): 8.2x NTM EBITDA

The consortium paid a discount to Take-Two’s premium valuation but a meaningful premium to distressed European comparables, suggesting a fair entry multiple for a control premium transaction. The critical question for PIF’s investment return centers on exit multiple expansion—achievable through revenue growth and margin improvement, but contingent on successful operational execution under the levered capital structure.

INVESTMENT IMPLICATIONS AND RATING FRAMEWORK

For EA public shareholders, the investment decision is straightforward: accept the $210 per share tender offer upon CFIUS approval. The current stock price of $203.79 implies a 3% deal spread, which does not adequately compensate retail investors for regulatory approval uncertainty or extended timeline risk.

The more nuanced strategic question concerns sector positioning following EA’s delisting. The transaction removes $55 billion in market capitalization from the publicly traded gaming sector, increasing scarcity value for remaining pure-play publishers. Take-Two Interactive emerges as the primary beneficiary, becoming the largest independent U.S.-based publisher following EA’s take-private and Activision Blizzard’s 2023 acquisition by Microsoft.

For credit investors evaluating the post-LBO debt package, the senior secured tranches offer adequate downside protection given EA’s intellectual property moat and recurring live service revenue streams. However, mezzanine debt and junior tranches carry elevated risk given execution uncertainty around margin expansion initiatives and potential consumer backlash to monetization changes.

UPGRADE TRIGGER: If PIF achieves >$600 million in annual cost savings within 18 months while maintaining franchise development quality and DAU/MAU stability, the de-levering trajectory would support credit rating upgrades and create positive exit multiple expansion opportunity.

DOWNGRADE TRIGGER: If workforce reductions exceed 25% of headcount, triggering talent exodus and franchise execution delays, or if monetization intensity drives >10% DAU decline across live service portfolio, debt service coverage would compress and credit quality would deteriorate meaningfully.

CATALYSTS TO MONITOR

• April-May 2026: CFIUS filing timeline disclosure and EA Q4 FY2026 earnings call commentary on regulatory progress

• June 2026: Target transaction close (Q1 FY2027 ends June 30)

• Q3 2026: First post-LBO workforce restructuring announcements (if deal closes)

• Q4 2026: EA Sports FC annual release monetization changes and holiday season performance under PIF ownership

The EA-PIF transaction represents an inflection point for gaming industry capital structure norms, with the $20 billion debt package and 93.4% sovereign wealth fund ownership creating a novel operating model for a major Western publisher. The regulatory approval timeline and post-close operational execution will determine whether this LBO structure becomes a template for future gaming industry consolidation or serves as a cautionary case study in over-leverage and cultural friction.

INVESTMENT DISCLAIMER

This analysis is provided for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other sort of advice. Press Play Finance (PPF) and the author, Taimoor Khan, are not registered investment advisors or broker-dealers.

The information presented in this article is based on publicly available sources and the author’s independent analysis. While every effort has been made to ensure accuracy, PPF makes no representations or warranties regarding the completeness or accuracy of the information provided.

Investing in securities involves risk, including the possible loss of principal. Past performance is not indicative of future results. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions.

The author and Press Play Finance may or may not hold positions in the securities discussed. This article should not be considered a recommendation to buy, sell, or hold any security mentioned herein.

ABOUT THE AUTHOR

Taimoor Khan is the founder and editor of Press Play Finance, a B2B finance publication delivering institutional-grade equity analysis of publicly listed video game companies. His coverage focuses on capital allocation, margin dynamics, and regulatory developments in the gaming sector.

© 2026 Press Play Finance. All rights reserved.

That’s a really thorough breakdown of the CFIUS timeline – it’s interesting to see how the debt load is going to impact future margins after the LBO.

Thank you. We hope that our coverage reaches out to people like you on a regular basis 🙂